We thought the “I don’t invest unless I can drive to the company” mantra had left Sand Hill Road a few years ago. The venerable firms have opened offices in outposts like Beijing and Bangalore. Other cities tout their own “Valley-like” ecosystem, the Silicon Alley, Prairie, Roundabout, Beach, Tundra, fill-in-the-regional blank. Coding skills are spreading globally: the TopCoder 2013 Open coding contest included entrants from 152 countries. Incubator spaces sprout like Starbuck’s on every urban corner. Competing in a business plan competition seems to now be a requirement for an undergraduate degree in any discipline.

Yet, a look at the late-stage dollar flow over the past three years suggests investors are creatures of habit. Growth stage investors are piling capital into the companies they know the most about – those that are near offices in Menlo and Palo Alto.

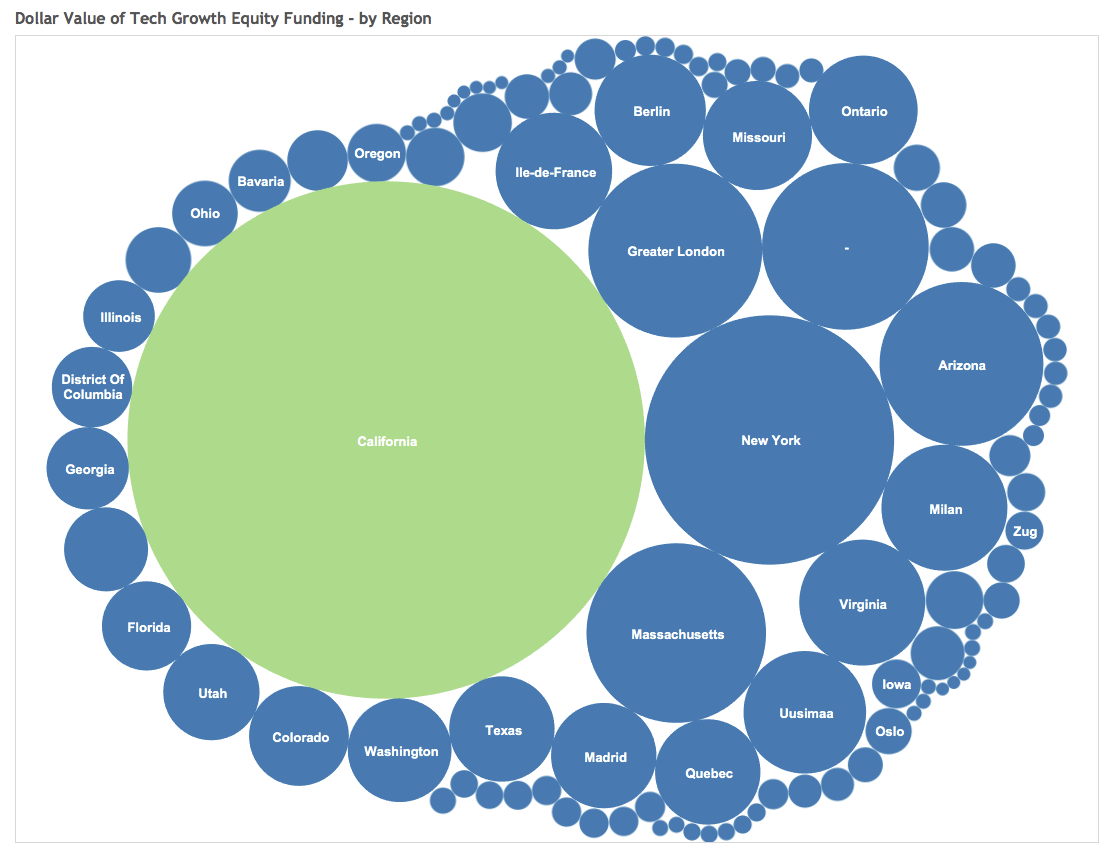

The above chart is the aggregate dollar volume over the past three years of venture growth rounds and private equity recapitalizations in North America and Europe. California companies absorbed 36.4% – more than a third – of all the private growth equity going into the tech economy in the Western Hemisphere.

The Valley ecosystem is special and unique, but this is not long-term healthy for the industry. I believe growth equity investors can generate differentiated returns by finding interesting ideas not subject to the “next unicorn” mentality (example here) by looking harder at companies outside California. To be clear, there are a lot of smart, experienced people in the Valley running important companies, but there are proportionately too many local dollars chasing those businesses. There are also smart, experienced people running companies in other geographies. ExactTarget, built in Indianapolis, provided its investors an attractive return when Salesforce purchased the company for $2.5 billion. Wayfair in Boston looks like an attractive outcome for its private investors as it heads for the public markets. AirWatch, built in Atlanta, turned $225M into $1.5 Billion.

If you are building a cool company outside the 408 and 650 area codes you are going to have be a little bit better at getting investor attention. We hear young companies from other geographies talk about relocating the business to get access to capital. It strikes me as foolish that in this virtual age an entreprenuer would have to uproot the core founding team and in the process lose key early employees to gain access to capital. We need better late stage ecosystems outside the Valley with investors willing to be equally aggressive on terms. We also need folks on Sand Hill Road to extend the ecosystem across North America and Western Europe, not just to Asia. There is plenty of capital in the asset class to support growth companies without moving them all to South San Francisco.